Three days ago, the SEC did something I genuinely didn't think would happen this fast.

On March 17, 2026, the Securities and Exchange Commission and the Commodity Futures Trading Commission published a joint 68-page interpretive release that explicitly names Solana as a digital commodity. Not a security. A commodity. The same bucket as Bitcoin and Ethereum.

That's not a leaked memo or a commissioner's off-the-cuff remark at a conference. It's a final agency statement that carries the full weight of federal regulatory law.

I've been holding SOL since 2021. Watched it crater to $8 during the FTX collapse. Watched the SEC name it as a security in the Binance lawsuit. Watched the lawsuits pile up and the institutional money stay on the sidelines. And now I'm watching the same agency that tried to kill Solana's legitimacy formally declare it a commodity.

If that doesn't make you at least a little suspicious about the timing, you haven't been paying attention to how Washington works.

But suspicion aside, the ruling is real, it's binding, and it changes the math for every SOL holder, every fund manager eyeing crypto, and every exchange that spent the last three years lawyering up. Here's what actually happened, what it means, and what most articles covering this are getting wrong.

What the SEC and CFTC actually said

The 68-page document creates a five-category taxonomy for crypto assets. This is the first time either agency has put formal definitions on paper, and it's worth understanding the full picture before zooming into Solana.

The five categories:

- Digital commodities -- crypto assets whose value comes from the operation of a functional system plus supply and demand. Not dependent on a central issuer's management. Think: decentralized networks with real usage.

- Digital collectibles -- NFTs, basically. Unique blockchain assets with distinct individual value.

- Digital tools -- utility tokens that function within a specific system. Not commodities, not securities.

- Stablecoins -- could be securities or not, depending on their structure and issuer claims. USDC and USDT aren't automatically safe.

- Digital securities -- tokenized versions of traditional financial instruments. Stocks, bonds, treasuries on a blockchain. These stay under SEC jurisdiction.

Only that last category -- digital securities -- remains fully under the SEC's regulatory umbrella. Everything else either falls to the CFTC or sits in a grey zone that the new Joint Harmonization Initiative is supposed to sort out.

The 16 named digital commodities: Bitcoin, Ethereum, Solana, XRP, Cardano, Chainlink, Avalanche, Polkadot, Hedera, Litecoin, Dogecoin, Shiba Inu, Tezos, Bitcoin Cash, Aptos, and Stellar.

That's a wild list if you think about it. Shiba Inu -- a memecoin that started as a joke -- now has the same federal classification as Bitcoin. The r/CryptoCurrency reaction thread had people genuinely confused about whether the SHIB inclusion was satire. It wasn't. I don't know if that says more about SHIB or about how broad this framework is.

Six days that changed crypto regulation

The interpretive release didn't come out of nowhere. On March 11, six days earlier, the SEC and CFTC signed a Memorandum of Understanding establishing a Joint Harmonization Initiative. The MOU is co-led by Robert Teply at the SEC and Meghan Tente at the CFTC, and it commits both agencies to coordinating on everything from product definitions to enforcement.

That MOU was the setup. The 68-page release was the punchline.

For anyone who lived through the Gensler era at the SEC (2021-2025), this is whiplash. Gary Gensler's SEC called pretty much everything except Bitcoin an unregistered security. Solana was specifically named in the 2023 Binance lawsuit. The entire DeFi ecosystem was operating under threat of enforcement action. And now? The same agency says most crypto isn't securities at all.

I'm not complaining. But the pivot is fast enough to give you vertigo.

Why this matters more for SOL than the other 15

Bitcoin and Ethereum were already treated as commodities in practice. Nobody seriously argued BTC was a security. ETH had the Hinman speech from 2018 (legally meaningless but widely cited). Those two didn't need this ruling.

Solana did.

SOL was in genuine regulatory purgatory. The SEC had named it as a security in enforcement actions. Institutional investors couldn't touch it without legal risk assessments that cost six figures. ETF applications faced the threshold question: if SOL is a security, you can't wrap it in a commodity ETF structure. Period.

That cloud is gone now. And the market reacted immediately.

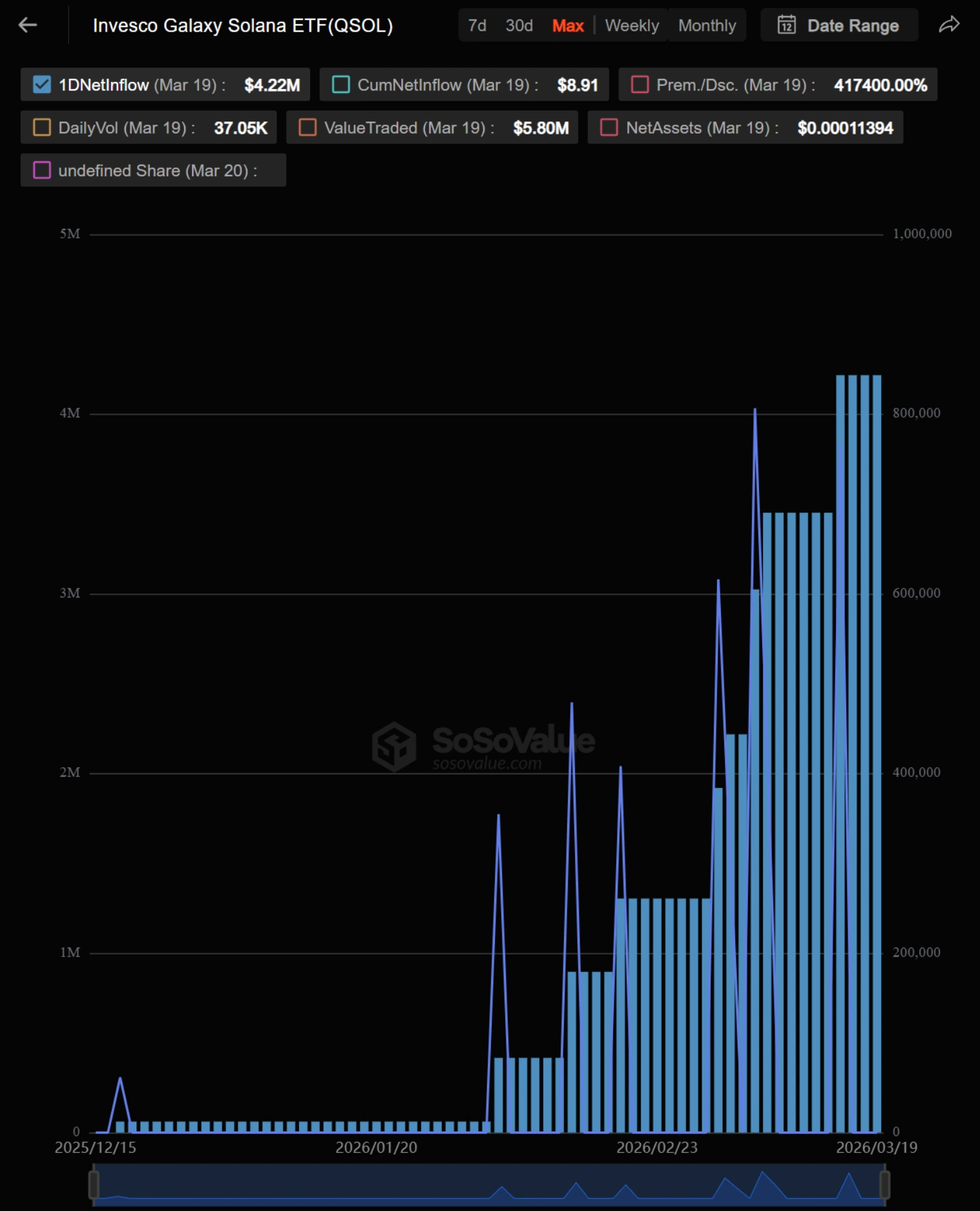

SOL jumped 22% from its March lows in the week following the announcement, hitting a one-month high near $97 before pulling back to around $90. Solana ETFs saw $17.81 million in inflows on March 17 alone -- the highest single-day net flow since early March. CoinCodex analysts are projecting $135 by May.

The r/solana subreddit was predictably euphoric, but the more interesting discussion happened in r/CryptoMarkets where traders debated whether the classification was already priced in from the MOU announcement six days earlier.

Honestly? The price reaction has been surprisingly muted given the magnitude of the news. When Bitcoin got its spot ETF approval in January 2024, BTC ran from $44K to $73K in two months. SOL got commodity classification and moved 22%. That tells me either the market had already priced most of this in, or the real move comes later when institutional products actually launch.

I think it's the latter.

The ETF question is now answered

SOL spot ETFs were already approved in October 2025 -- Solana was only the third crypto to get that treatment after Bitcoin and Ethereum. Trading started October 28, and by December, 50% of Solana ETF holders were 13F institutional filers. That's a staggering adoption rate compared to XRP ETFs where institutional holders were under 15%.

But there was always this legal asterisk hanging over everything. If the SEC later decided SOL was a security, those ETFs would face existential legal challenges.

That asterisk is gone.

Even better: the ruling explicitly states that on-chain staking is not a securities transaction. This is huge for Solana ETFs specifically because staking was built into the products from day one. Bitwise's BSOL stakes 100% of its SOL holdings, targeting 7%+ annual staking rewards. That's a yield component that Bitcoin and Ethereum ETFs can't match.

The REX-Osprey Solana Staking ETF (SSK) was actually first to market back in July 2025, and Bitwise's BSOL debuted with $56 million in first-day trading volume. Now there are filings for even more exotic products like VanEck's JitoSOL ETF, which holds a Solana liquid staking token.

If you've been watching this space through our crypto staking platforms breakdown, you already know that staking yields look great on paper until you factor in commission rates and inflation. The same applies to ETF staking -- fund managers take a cut of those rewards. But the regulatory green light makes the whole category legitimate in a way it wasn't before.

Staking is officially not a security (and that's bigger than you think)

This deserves its own section because the staking question has been hanging over the entire proof-of-stake ecosystem for years.

Under the Gensler SEC, Kraken paid a $30 million fine for its staking-as-a-service program. Coinbase received a Wells notice partly over staking. The implicit message was: if you offer staking to customers, you might be offering unregistered securities. That context matters if you're comparing centralized platforms now, which is why our best crypto exchanges guide spends time on staking access and regulatory posture instead of just headline trading fees, and the focused Kraken vs Coinbase comparison separates exchange choice from the staking decision.

The March 17 ruling says the opposite. Explicitly. On-chain staking, mining rewards, and airdrops of digital commodities are not securities transactions.

For Solana specifically, this is massive. SOL's staking rate is around 65% of circulating supply. The network's economic security model depends on widespread staking participation. If staking were classified as a securities activity, every validator, every liquid staking protocol, every DeFi product built on staked SOL would have been operating in a legal minefield.

That minefield just got deactivated. Not by a court ruling that could be appealed, not by a no-action letter that could be rescinded -- by a joint interpretive release from both federal regulators.

Whether you're running a validator, staking through an exchange, or using liquid staking tokens like JitoSOL, you now have the clearest legal ground the U.S. has ever provided. And if you're holding SOL on a centralized exchange like those in our no-KYC exchange roundup, the staking options those platforms offer just got materially less risky from a regulatory standpoint.

What the cheerleaders aren't telling you

OK so here's where I put on the skeptic hat, because every other article I've read about this ruling reads like a press release from a Solana venture fund.

First: this is an interpretive release, not legislation. Congress hasn't passed a comprehensive crypto market structure bill. The FIT21 Act is still bouncing around. An interpretive release can be modified or reversed by a future administration. If the political winds shift and a Gensler 2.0 takes over the SEC in 2029, this taxonomy could be revised.

It won't be easy to reverse -- these things build legal precedent and market reliance. But "can't be reversed" and "probably won't be reversed" are different things.

Second: "digital commodity" doesn't mean "unregulated." CFTC oversight comes with its own compliance requirements. Anti-fraud and anti-manipulation authority still applies. Exchanges dealing in digital commodities will still need to register and comply. This isn't a free-for-all.

Third: the 16 named assets aren't the only ones that could qualify. The taxonomy provides criteria, not just a list. But if your favorite altcoin didn't make the cut, that doesn't automatically make it a security either. It means you're in ambiguity. And ambiguity in regulatory frameworks is where lawsuits come from.

Fourth -- and this is the one nobody's talking about -- the stablecoin category is deliberately vague. The ruling says stablecoins "may or may not be securities depending on their structure." USDC and USDT didn't get named as commodities. For an ecosystem that runs on stablecoin liquidity, that's a gap worth watching.

So what should you actually do?

If you're holding SOL, the regulatory risk premium just dropped significantly. That doesn't mean SOL is going to $200 tomorrow. Markets are weird, macro conditions matter, and crypto has a way of finding new things to panic about.

But the structural argument for SOL got meaningfully stronger. Institutional access is clearer. ETF products have legal certainty. Staking is explicitly blessed. And Solana's network metrics -- over 4,000 TPS in practice, sub-cent transaction fees, a DeFi ecosystem that's second only to Ethereum -- now exist in a regulatory environment that doesn't threaten to shut them down.

If you're holding SOL on an exchange and not staking, you're leaving yield on the table. The regulatory excuse for not staking just evaporated. Whether you stake through an exchange, a hardware wallet, or a liquid staking protocol, the math now favors participation.

If you're thinking about getting exposure for the first time, the ETF route is the simplest for traditional investors. Bitwise BSOL gives you spot SOL exposure plus staking yield in a standard brokerage account. No wallet setup, no seed phrases, no bridge exploits to worry about. If you'd rather buy SOL directly and manage it yourself, Bybit has some of the lowest spot trading fees in the industry and supports SOL staking natively -- we covered the full breakdown in our Bybit review. For self-custody, our hardware wallet guide covers the best options for holding SOL securely.

And if you're a trader who's been waiting for regulatory clarity before sizing up, March 17 was your signal. The question isn't whether Solana is a commodity anymore. The question is what you do with that information.

The real story is the framework, not Solana

I've spent most of this article on SOL because that's what readers are searching for. But honestly? The bigger story is the framework itself.

For the first time in crypto's 15-year existence, the two primary U.S. financial regulators have jointly defined what different types of crypto assets are. They've drawn lines. They've named names. They've said staking and mining aren't securities activities.

That matters for every single crypto project, not just the 16 that made the commodity list. It matters for the DeFi protocols that were operating without knowing which regulator might come after them. It matters for the exchanges that spent millions on legal compliance for rules that didn't exist yet. It matters for the developers who moved offshore because building in the U.S. felt like building on a fault line.

Is the framework perfect? No. The stablecoin ambiguity is a problem. The "digital tools" category is vague. And interpretive releases aren't as durable as legislation.

But compared to "everything might be a security and we'll tell you which ones through enforcement actions"? This is progress. Real, tangible, write-it-into-your-investment-thesis progress.

If you're looking to track how your SOL holdings perform alongside other assets following this regulatory shift, our crypto portfolio tracker comparison covers tools that connect to most major exchanges and wallets. And for anyone with crypto gains from 2025 who's now thinking about tax implications of staking rewards, we broke down the best crypto tax software for the new 1099-DA era.

Bottom line

The SEC classified Solana as a digital commodity on March 17, 2026. It's not a security. Staking is legal. ETFs have clear legal ground. Institutional access just got simpler.

SOL's regulatory risk dropped from "we might sue you" to "you're a commodity, figure it out with the CFTC." That's a massive shift, even if the price hasn't fully reflected it yet.

I'm not selling my SOL. I wasn't going to anyway, but now I can hold it without wondering if the SEC is going to file another lawsuit that craters the price by 40% overnight. That peace of mind is worth something, even if it doesn't show up on a chart.

The real test comes over the next 6-12 months. Will institutional money actually flow in? Will Congress pass legislation that makes this framework permanent? Will the stablecoin question get resolved? Those are the dominoes that matter now.

For the first time in a while, though, the dominoes are falling in the right direction.

Frequently Asked Questions

Ready to check Solana?

Use the verified route if the trade-offs still fit. If not, jump back to the summary and compare the alternatives.

Crypto and productivity editor focused on cost, custody risk, setup friction, exports, fees, and workflow drag. Prioritizes verifiable numbers and clear skip criteria over hype.

Lucas starts with total operating cost, then ranks tools by setup and recurring friction, custody or export, reversibility, and whether the decision still makes sense when the exit path is included.

Related Articles

Stablecoin Cards Compared: Rewards, FX, and Custody Traps

Stablecoin-funded payment cards compared by everyday spend cost, reward caps, FX and conversion fees, custody model, region availability, and tax friction

Coinbase Card, Bybit Card, Crypto.com Prepaid Card, and Nexo Card compared by stablecoin spend cost, rewards, FX fees, custody, and region fit.

MoonPay vs Transak vs Ramp: Which Crypto On-Ramp Costs Less?

3 crypto fiat on-ramp providers compared by fee clarity, payment rails, wallet delivery, partner markup risk, and buyer fit

MoonPay, Transak, and Ramp Network compared by official fee disclosures, payment rails, partner markups, KYC caveats, and wallet-delivery fit.