The lazy Bitcoin DCA answer is "just automate it." That skips the part where the app decides how much of every buy actually becomes Bitcoin, how quickly you can withdraw it, and whether your sats sit in a custody setup you understand.

My default pick is River for a US buyer whose main job is scheduled Bitcoin accumulation. It wins because the fee rule is simple enough to model, the product stays Bitcoin-only, and the public Proof of Reserves page gives buyers one more thing to verify instead of just trust.

Strike is the better app if Bitcoin is also how you move money. Swan is the better fit when guided custody, IRA, Vault, or Private-style support matters more than squeezing the DCA fee to the floor. That is the useful split. Not "which app looks the most Bitcoin-native?" All three can say that.

I checked official fee/support pages, River reserve material, current SERP competitors, GDT operator data, and concrete r/Bitcoin and r/BitcoinBeginners question patterns. I did not create accounts, link a bank, place a recurring buy, preview spreads, send a withdrawal, test Lightning, or open support tickets. This is a buying decision guide, not a live account test.

If you still need a general exchange first, start with our best crypto exchanges guide or the narrower Kraken vs Coinbase comparison. If the plan is to buy Bitcoin here and hold it for years, pair this with our hardware wallet guide and seed phrase backup comparison before the balance gets meaningful.

-

#1 RiverBest default for US Bitcoin DCA: zero-fee recurring buys after the initial period and public Proof of Reserves

-

#2 StrikeBest if you want DCA plus Lightning, payments, free auto-withdrawals, and broader money movement

-

#3 Swan BitcoinBest if guided Bitcoin custody, Swan Vault, IRA, or Private support matters more than lowest simple DCA cost

If I were setting up a boring weekly Bitcoin buy for a friend, I would start with River . If that friend used Bitcoin payments, Lightning, or international transfers, I would compare Strike before deciding. If they wanted help with custody choices or a Bitcoin IRA, I would make Swan the specialist check.

River vs Strike vs Swan comparison table

| Feature | River | Strike | Swan Bitcoin |

|---|---|---|---|

| Best job | US Bitcoin DCA and long-term accumulation | DCA plus Bitcoin payments and withdrawals | Guided custody, IRA, Vault, and serious long-term support |

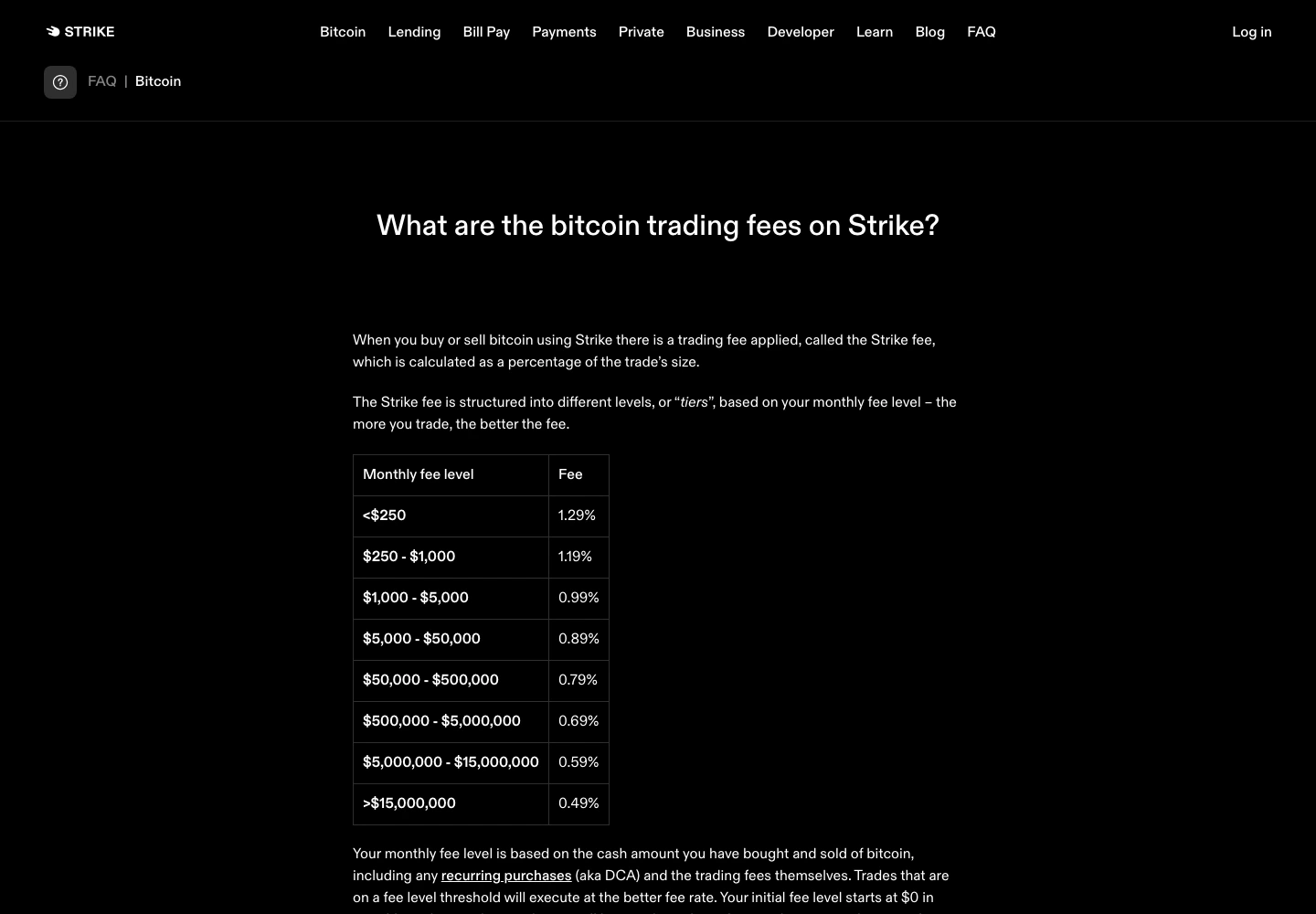

| Recurring buy rule | Zero fees after day 7 for daily/hourly, or from the 2nd weekly order | No-fee DCA after first week or from 2nd weekly/monthly purchase | Current help page says 1% on buys and sells |

| One-time buy rule | 1% up to $1M; lower tiers above that | Tiered fees starting at 1.29% in the checked FAQ | Same 1% buy/sell fee in the checked support article |

| Custody signal | Public Proof of Reserves and full-reserve Bitcoin custody claim | Says cash and Bitcoin are fully backed; licensed disclosures are visible | Swan Safe, Swan Vault, Swan Guard, and custody partners are the story |

| Withdrawal angle | Good self-custody fit; verify current send timing and limits before funding | Auto-withdrawals and free flexible on-chain withdrawal path are the draw | Auto-withdrawal can waive Swan Safe custody fees when enabled |

| Skip if | You need payments/Lightning-first utility or non-US coverage | You want a pure accumulation app with reserve proof as the lead trust signal | Lowest simple DCA cost is the only thing you care about |

| Action | Compare River | Compare Strike | Compare Swan |

How I ranked these Bitcoin DCA apps

The ranking uses one rubric: DCA Cost, Custody Clarity, Withdrawal Path, Buyer Fit, and Caveat Clarity. DCA Cost asks whether the recurring-buy rule is easy to model. Custody Clarity asks whether the buyer can understand who holds what. Withdrawal Path asks how naturally the product pushes coins toward self-custody. Buyer Fit asks whether the tool matches the person behind this search. Caveat Clarity punishes "free" language when the official fine print still matters.

That last one matters more than people think. A Bitcoin-only app can still make the wrong buyer pay the wrong bill. The expensive mistake is not choosing a "bad" app. It is choosing a payments app when you wanted a quiet accumulation machine, or choosing a guided custody platform when you really wanted the cheapest weekly buy.

Start with the job.

The Bitcoin DCA fee trap is comparing the wrong transaction

Most fee comparisons get weird because they compare a one-time buy on one app against a recurring-buy rule on another. That is not a fair fight. River's standard one-time fee is not the same product as River's recurring buy after the initial period. Strike's first fee tier is not the same product as Strike's no-fee DCA path. Swan's 1% buy/sell line is straightforward, but it sits next to custody products that can change the real bill if you leave Bitcoin in the account.

So I am not ranking these by the lowest number printed on a page. I am ranking them by the workflow a buyer will actually use. If you will buy once a quarter in larger chunks, River and Strike's one-time fee rows matter more. If you will buy every week and withdraw later, the recurring-buy waiver and withdrawal path matter more. If you want a person or custody service helping with IRA, Vault, or account structure, Swan's extra service depth can be worth paying for.

The second trap is pretending the buy button is the finish line. It is not. The app should get Bitcoin into the buyer's long-term plan without creating a mystery around cost basis, pending funds, withdrawal timing, or custody. A cheap app that makes self-custody feel optional for too long can still become expensive.

1. River: best default for scheduled Bitcoin accumulation

River wins because its core DCA promise is easy to explain and easy to audit against official docs. The official River fee article updated May 15, 2026 says one-time buy/sell orders up to $1,000,000 use a 1.00% River fee, while recurring buys become zero-fee after the initial period: day eight onward for daily or hourly orders, and the second order onward for weekly recurring buys.

That is the kind of rule a normal person can plan around. Set the recurring buy, survive the initial standard-fee order, and then the explicit River fee drops to zero for the recurring lane. River also says the buy/sell price may include a spread. So no, "zero fee" does not mean "the platform has no economics." It means the explicit recurring fee is waived under the stated rules.

The reason I put River first is not just cost. River's public Proof of Reserves page is a better trust signal than vague "secure custody" copy. The current public material says River proves it holds 100% of Bitcoin deposits in full reserve, and the page exposes assets, liabilities, and monthly reserve ratios. That does not replace self-custody. It does make the custody claim more inspectable while your Bitcoin is still on the platform.

River also has a direct-deposit angle that matters for a specific buyer. The same fee article says automatic payroll conversions can be fee-free up to $30,000 per account title per month when they are set to convert automatically. That is not the default use case for everyone, but it gives River a cleaner "set the habit and leave it alone" story than most general exchanges.

Where River can be wrong is utility. If your Bitcoin app also needs to handle day-to-day Lightning payments, cash movement, or international transfer behavior, River's quieter product can feel like the narrow lane. I do not count that against River for a DCA buyer. I do count it against River for anyone who wants one Bitcoin app to become a spending and transfer tool.

River is not the universal answer. It is US-focused, less payments-centered than Strike, and not the place I would send someone who wants IRA or Vault guidance. It also does not remove the tax-lot problem. A weekly buy creates a pile of transactions, so use our crypto tax software guide or the CoinLedger vs Koinly comparison before April becomes a spreadsheet crime scene.

Use River if the plan is boring: buy Bitcoin on a schedule, verify the fee rules, withdraw when your self-custody setup is ready, and stop staring at the app.

River combines an official zero-fee recurring-buy path after the initial period with public Proof of Reserves, which is rare among consumer Bitcoin apps.

Skip it if you need Lightning-first spending, international payments, Swan-style guided custody, or non-US availability.

River ranks first because the recurring-buy rule and reserve proof fit the default DCA buyer better than Strike's payments focus or Swan's custody-service cost model.

- Official fee page says recurring buys become zero-fee after the initial period

- Public Proof of Reserves gives a concrete custody claim to inspect

- Bitcoin-only positioning keeps the app from turning into an altcoin menu

- Strong fit for a simple weekly or daily accumulation habit

- One-time orders still use the standard fee schedule

- River says buy and sell prices may include a spread

- Not the strongest pick if Lightning payments are part of the job

- No account setup, live spread preview, withdrawal, or support workflow was tested here

2. Strike: best when DCA and payments share the same wallet

Strike is the app I would pick if Bitcoin is not just something you buy, but something you move. The official Bitcoin product page pushes low-fee buying, no-fee recurring purchases, target orders, free withdrawals, Lightning, payments, bill pay, and global transfers. That is a broader job than River.

The fee page I checked is specific. Strike's FAQ says one-time Bitcoin buys and sells use tiered fees based on monthly trading volume, starting at 1.29% below $250 in monthly trading volume and stepping down as volume rises. It also says Bitcoin trading fees do not apply to recurring purchases after the first week for hourly and daily purchases, or starting with the second purchase for weekly and monthly purchases. Businesses are excluded from that waiver.

That makes Strike cheaper than the first fee row suggests if you actually use recurring buys. The catch is behavioral. If you keep smashing one-time buys, the fee table matters. If you set a schedule, the DCA waiver matters. If you also use Lightning, auto-withdrawals, bill pay, or transfers, River starts to look too narrow.

I would not make Strike the default for a person who only wants a quiet accumulation lane and reserve-proof transparency. Strike is busier. That is not bad. It is just a different product. It is closer to a Bitcoin money app than a pure stacking app.

Use Strike if the buyer says, "I want to buy Bitcoin every week, withdraw it, and maybe use Lightning or payments later." Skip it if every extra feature is just a distraction.

Strike is the best fit when recurring Bitcoin buys and free withdrawal/payment features belong in the same app.

Skip it if you want the simplest Bitcoin-only accumulation app and public reserve proof is a top requirement.

Strike ranks second because it is more versatile than River, but the broader payments workflow is extra complexity for the default DCA-only buyer.

- Official FAQ says recurring Bitcoin purchases can avoid trading fees after the initial period

- Better than River if Lightning, free auto-withdrawals, bill pay, or global transfers matter

- Tiered fee table is public and easy to compare against one-time-buy habits

- NMLS and New York virtual-currency license disclosures are visible in the public footer

- First-tier one-time trading fee was 1.29% on the checked FAQ page

- The app has more payment features than a pure DCA buyer may need

- Fully backed language is useful, but it is not the same as River's public Proof of Reserves workflow

- No live app fee tracker, spread preview, withdrawal, or Lightning workflow was tested here

3. Swan Bitcoin: best when custody help matters more than the cheapest DCA lane

Swan loses the default DCA-cost slot. That does not make it useless.

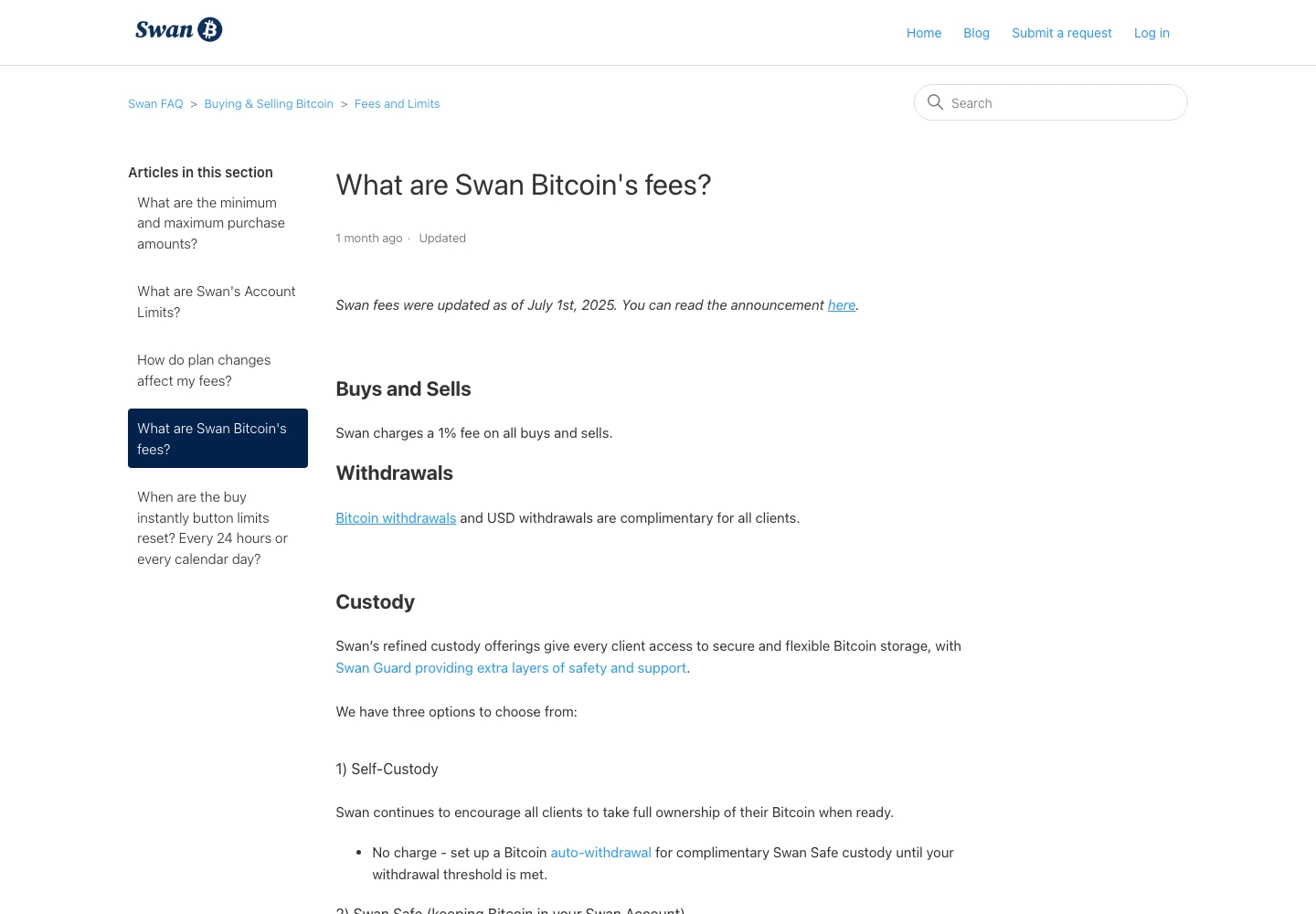

The current Swan help page I checked was updated April 22, 2026 and says Swan charges a 1% fee on buys and sells. The same page is where the real Swan decision shows up: Swan Safe, Swan Vault, Swan Guard, Swan IRA, Private, Business, custody partners, and monthly assets-on-platform fees when balances stay in certain custody setups.

For example, the checked Swan page listed Swan Vault at a 0.02% monthly assets-on-platform fee with a $30 monthly minimum and $500 monthly maximum, while Swan IRA used the same monthly rate with a $20 minimum. Those lines matter only if that custody or IRA workflow is part of the job.

That is a different product shape. River and Strike are easier to justify when the job is "buy Bitcoin on repeat and withdraw it." Swan gets more interesting when the buyer wants guidance, IRA context, collaborative multisig, or a more assisted custody path. The tradeoff is that those extra services bring fee lines the buyer has to model.

The most important Swan detail is the self-custody incentive. The help page says Swan Safe has a 0.03% assets-on-platform monthly fee for clients who keep Bitcoin in their Swan account, but it also says the fee is waived for clients with Bitcoin auto-withdrawals enabled. That is good product pressure. It nudges the buyer toward self-custody instead of silently monetizing inertia.

My issue with Swan as the default is narrower: a buyer searching River vs Strike vs Swan is often comparing simple recurring buys. If that is the whole job, Swan asks them to pay more for a service stack they may not need. If the buyer actually wants IRA, Vault, Private, guided onboarding, or custody help, Swan deserves the third slot. Not the first.

Use Swan if you want the support and custody ecosystem. Skip it if you only want the cheapest automated weekly purchase.

Swan is less compelling for cheapest DCA, but stronger when the buyer values Swan Safe, Vault, IRA, Private, or guided custody support.

Skip it if you only want the lowest-cost recurring buy path and plan to self-custody without guided help.

Swan ranks third because its custody ecosystem is useful, but the current buy/sell and custody fee model is harder to justify for a simple DCA-only buyer.

- Current help page makes the 1% buy/sell fee explicit

- Swan Safe, Swan Vault, Swan IRA, and Swan Private give serious stackers more service depth

- Auto-withdrawal language can waive Swan Safe custody fees when enabled

- Better fit than River or Strike for buyers who want guided custody decisions

- Pure DCA buyers can usually model a cheaper recurring-buy lane with River or Strike

- Custody products introduce monthly assets-on-platform fees the buyer must understand

- The service stack can be overkill for someone who only wants a weekly buy and withdrawal habit

- No account setup, custody onboarding, IRA workflow, Vault setup, or support interaction was tested here

Also considered: Coinbase, Kraken, and Cash App

I left the big general exchanges out of the ranked list on purpose. Coinbase and Kraken are already covered in our broader exchange coverage, and they are better compared when the buyer wants multi-asset access, order-book trading, or a mainstream regulated exchange rather than a Bitcoin-only accumulation lane.

Cash App is useful for casual Bitcoin buying, but this article is not trying to pick the easiest consumer finance app. It is trying to pick the cleaner repeat-buy workflow among three Bitcoin-native names. The minute you care about long-term custody, withdrawal habits, and recurring purchase economics, the River vs Strike vs Swan fork is the sharper buyer question.

How to choose the right Bitcoin DCA app

Start with the failure you are trying to avoid. If the failure is paying avoidable explicit DCA fees, start with River. If the failure is needing a second app for Lightning, free withdrawals, or payments later, compare Strike. If the failure is trying to design custody alone when you really want guided help, compare Swan.

Do not pick based on "Bitcoin-only" branding alone. All three can pass that vibe check. The real decision is what happens after the first buy. Does the app make recurring buys cheaper? Does it make withdrawals easy enough that you will actually use self-custody? Does the custody model make sense if you leave a balance there for a while? Does the app create a tax-log mess you are ready to handle?

My practical rule: River for the default DCA buyer, Strike for the payments-plus-DCA buyer, Swan for the guided-custody buyer. If none of those labels fits, you probably need a broader exchange comparison before choosing a Bitcoin-only app.

Final verdict: River wins the default DCA decision

River is my default recommendation in River vs Strike vs Swan because it fits the narrow buyer job best: scheduled Bitcoin accumulation with an official zero-fee recurring-buy path after the initial period and public reserve proof while balances sit on-platform.

Strike is the strongest alternative. If you want DCA plus Lightning, auto-withdrawals, payments, bill pay, or global transfer utility, I would not force you into River just because it is cleaner. Strike is more useful when Bitcoin is also a payment rail.

Swan is the specialist. It is not my cheapest DCA pick, but it makes sense for buyers who want guided custody, IRA context, Vault, or Private-style help. The wrong buyer is the person paying for Swan's service depth while only needing a cheap weekly buy.

The counter-intuitive take: the best Bitcoin DCA app is the one you can stop thinking about. If the app keeps you fee-checking, app-hopping, and delaying self-custody, it is not saving time. It is turning a simple habit into a second job.

River is the best default for a US Bitcoin DCA buyer. Strike is better when payment utility matters. Swan is the custody-services specialist, not the cheapest simple recurring-buy lane.

Compare River