Unpopular opinion: most people reading "best crypto IRA" articles don't actually need a crypto IRA.

BlackRock's spot Bitcoin ETF (IBIT) charges 0.25% per year. You can buy it inside any Fidelity, Schwab, or Vanguard Roth IRA you already have. No special account. No setup fees. No 1% trading commissions. For Bitcoin-only exposure, the ETF route is objectively cheaper by a factor of four.

So why does this article exist? Because crypto IRAs solve problems ETFs can't. Altcoin access (Solana, Chainlink, 250+ tokens). Round-the-clock trading when ETFs close at 4 PM. Actual self-custody of your retirement Bitcoin through multisig vaults. And for people who want all of that inside a tax-advantaged wrapper, the options are better than ever. If you are specifically stuck on the new match-heavy app offer, read the focused Crypto.com IRA vs iTrustCapital comparison after this shortlist. The fees are still a minefield.

Five platforms, every fee verified on official docs in March 2026, and the compound math on what these fees actually cost over 10 and 20 years. One platform's fee structure is so bad it should come with a warning label.

-

#1 iTrustCapitalBest overall — 1% flat fee, no monthly charges, 90+ cryptos

-

#2 Fidelity Crypto IRABest for simplicity — use your existing Fidelity account, no custody fees

-

#3 UnchainedBest for self-custody — multisig vault, you hold the keys

Crypto IRA Fee Comparison — The Numbers That Matter

Every platform markets themselves as "low-fee." Here's what they actually charge when you read the fine print.

| Feature | iTrustCapital | Fidelity Crypto IRA | Alto CryptoIRA | Unchained | Bitcoin IRA |

|---|---|---|---|---|---|

| Trading Fee | 1% | 1% spread | 1% | 1.5% | ~2% |

| Setup / Monthly | None / None | None / None | None / None | $250/yr / None | 5.99% setup + 0.08%/mo |

| Minimum | $1,000 | None | $10 | $2,000/trade | $1,000 |

| Cryptos | 90+ | 5 | 250+ | BTC only | 75+ |

| Custody | Fireblocks (institutional) | Fidelity Digital Assets | Coinbase | Multisig (2 of 3 keys) | BitGo |

| Action | Visit iTrustCapital → | Visit Fidelity → | Visit Alto → | Visit Unchained → | Visit Bitcoin IRA → |

That table looks clean until you run the compound math. A 1% difference in annual fees on a $50,000 portfolio over 20 years costs you roughly $13,000 in lost growth. Bitcoin IRA's fee stack (2% trades plus monthly maintenance plus the upfront setup fee) can cost you over $30,000 on the same portfolio. I'll break this down platform by platform.

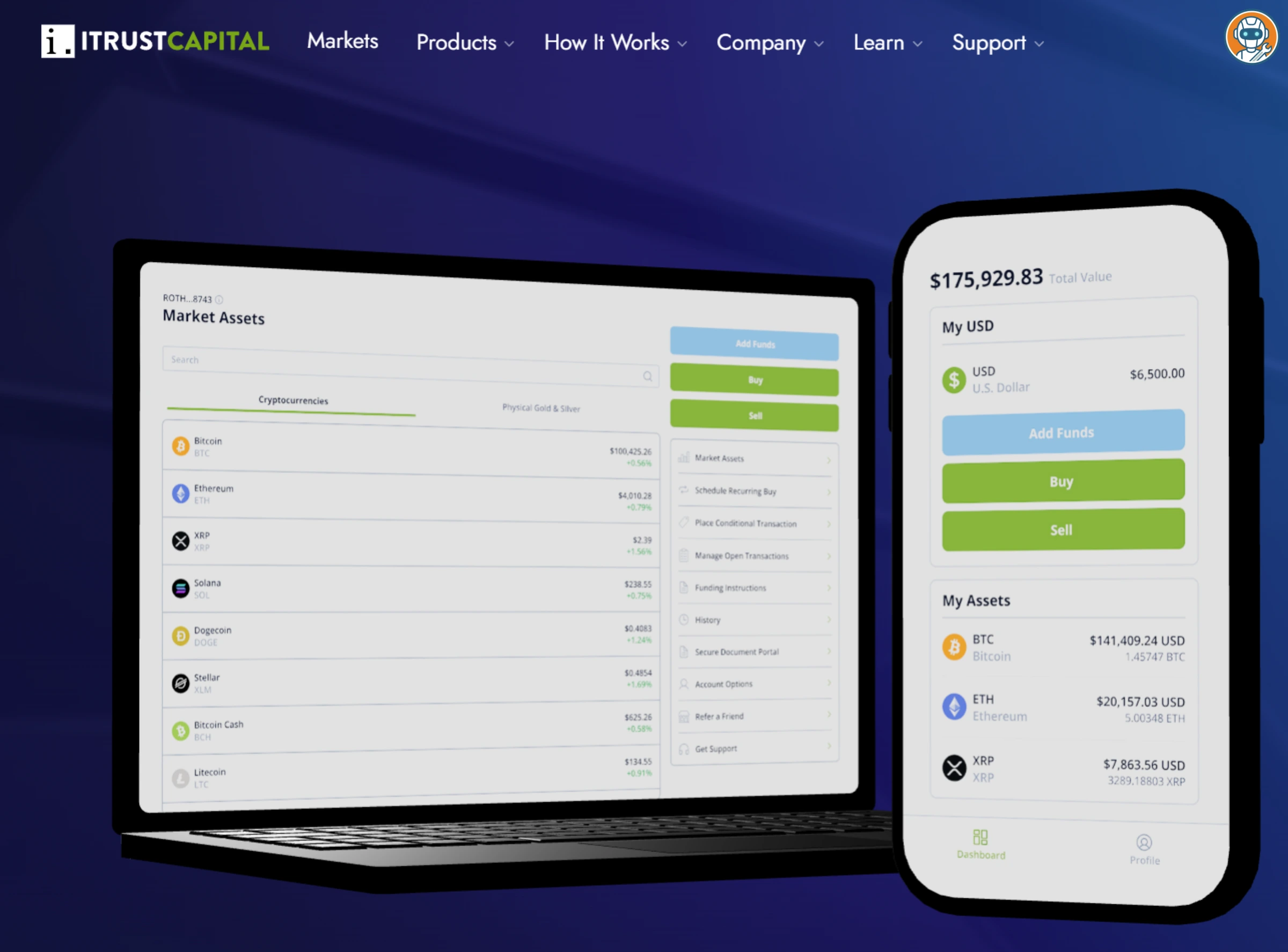

iTrustCapital — Best Overall Custodial IRA

iTrustCapital is what a crypto IRA should look like. Flat 1% per trade. No setup fee, no monthly fee, no annual maintenance fee, no hidden anything. After years of crypto platforms nickel-and-diming customers with hidden charges, iTrustCapital's pricing page is almost suspiciously straightforward.

Cleanest fee structure in the industry — flat 1% per trade with zero setup, monthly, or maintenance fees.

Anyone wanting self-custody — iTrustCapital holds all keys in their Fireblocks vault.

- Flat 1% trading fee with zero hidden charges

- No monthly or annual maintenance fees

- 90+ cryptocurrencies plus physical gold and silver

- A+ BBB rating — they actually respond to negative reviews

- Fireblocks institutional custody

- $1,000 minimum to open (higher than Alto's $10)

- No self-custody option — your keys, their vault

- $75 fee for Roth conversions

- Limited staking options compared to holding crypto directly

The 90+ supported cryptos cover all the majors (BTC, ETH, SOL, ADA, LINK, DOT) plus some mid-caps that Alto and Fidelity skip. They also offer physical gold and silver in the same IRA, which is a nice hedge option if you're the "prepare for everything" type.

One thing that doesn't get enough attention: iTrustCapital actively responds to BBB and Trustpilot complaints. That matters because withdrawal delays are the number-one complaint across every crypto IRA provider. At least with iTrustCapital, there's a public paper trail showing they address issues. Not perfect (one user reported a 30-day withdrawal delay involving XRP) but better than Bitcoin IRA's "we'll get back to you" approach.

Use iTrustCapital if you want a clean, low-fee custodial IRA with decent token selection. Skip it if you need 250+ altcoins (go Alto) or self-custody (go Unchained).

Fidelity Crypto IRA — The Boring Pick That Makes Sense

Fidelity launched their Crypto IRA and suddenly the "best crypto IRA" conversation changed entirely. Because here's the thing: millions of people already have a Fidelity IRA. Adding crypto exposure takes about five minutes. No new account. No new custodian. No new company to trust with your retirement money.

Use your existing Fidelity account to hold actual crypto alongside spot ETFs — zero new accounts, zero friction.

Altcoin investors or California residents — only 5 cryptocurrencies supported and not available in CA or OR.

- Zero account fees, zero custody fees, zero setup fees

- Uses your existing Fidelity brokerage account

- Fidelity Digital Assets custody — institutional-grade cold storage

- Also access spot crypto ETFs (FBTC, FETH, FSOL) in the same account

- Only 5 cryptocurrencies: BTC, ETH, SOL, LTC, and their FIDD stablecoin

- 1% spread baked into execution price — not obvious to casual users

- Not available in California or Oregon

- No altcoin access beyond the big names

The 1% spread is worth scrutinizing. Fidelity doesn't charge an explicit trading "fee." They embed it in the execution price. So when you buy Bitcoin at $95,000, you're actually paying around $95,950. Functionally identical to iTrustCapital's 1% fee, but less transparent. Reddit threads in r/fidelityinvestments have called this out repeatedly.

But here's why Fidelity still wins for a lot of people: you can hold spot crypto ETFs and actual crypto in the same IRA. Want $5,000 in IBIT (0.25% annual fee) for long-term Bitcoin exposure and $2,000 in actual SOL for the upside? Done. One account, one login, one tax document. Nobody else offers this flexibility.

Use Fidelity if you already have accounts there and want BTC/ETH/SOL exposure with zero friction. Skip it if you want altcoins or live in California.

Alto CryptoIRA — The Altcoin IRA

Alto exists for one reason: you want Chainlink, Arbitrum, Render, or any of 250+ tokens inside a tax-advantaged retirement account. Nobody else comes close on token selection.

250+ cryptocurrencies via Coinbase integration with a $10 minimum — the only IRA practical for small weekly DCA.

Anyone uncomfortable with Coinbase custody or who prefers Bitcoin-only self-custody solutions.

- 250+ cryptocurrencies via Coinbase integration

- $10 minimum investment — lowest in the industry by far

- No setup fees, no monthly fees

- 1% flat trading fee — same as iTrustCapital

- Coinbase custody means you're trusting Coinbase

- No self-custody option

- Limited educational resources compared to iTrustCapital

- Trustpilot reviews are mixed — some report slow customer support

The $10 minimum is genuinely impressive. Most crypto IRAs require $1,000+. If you're DCA-ing $50 a week into a diversified crypto basket inside your Roth IRA, Alto is the only platform that makes this practical. iTrustCapital won't let you in the door until you have $1,000.

The Coinbase dependency cuts both ways. You get access to Coinbase's massive token list and institutional custody infrastructure. But your crypto is on Coinbase. The same Coinbase that the SEC sued in 2023 (case still unresolved as of March 2026), the same Coinbase that handles custody for several Bitcoin ETFs. r/CryptoCurrency has... opinions about this. Most of them boil down to: "Coinbase is fine until it isn't."

Use Alto if altcoin diversity inside an IRA matters to you. Skip it if you're Bitcoin-only (iTrustCapital or Unchained are better) or if Coinbase custody makes you uncomfortable.

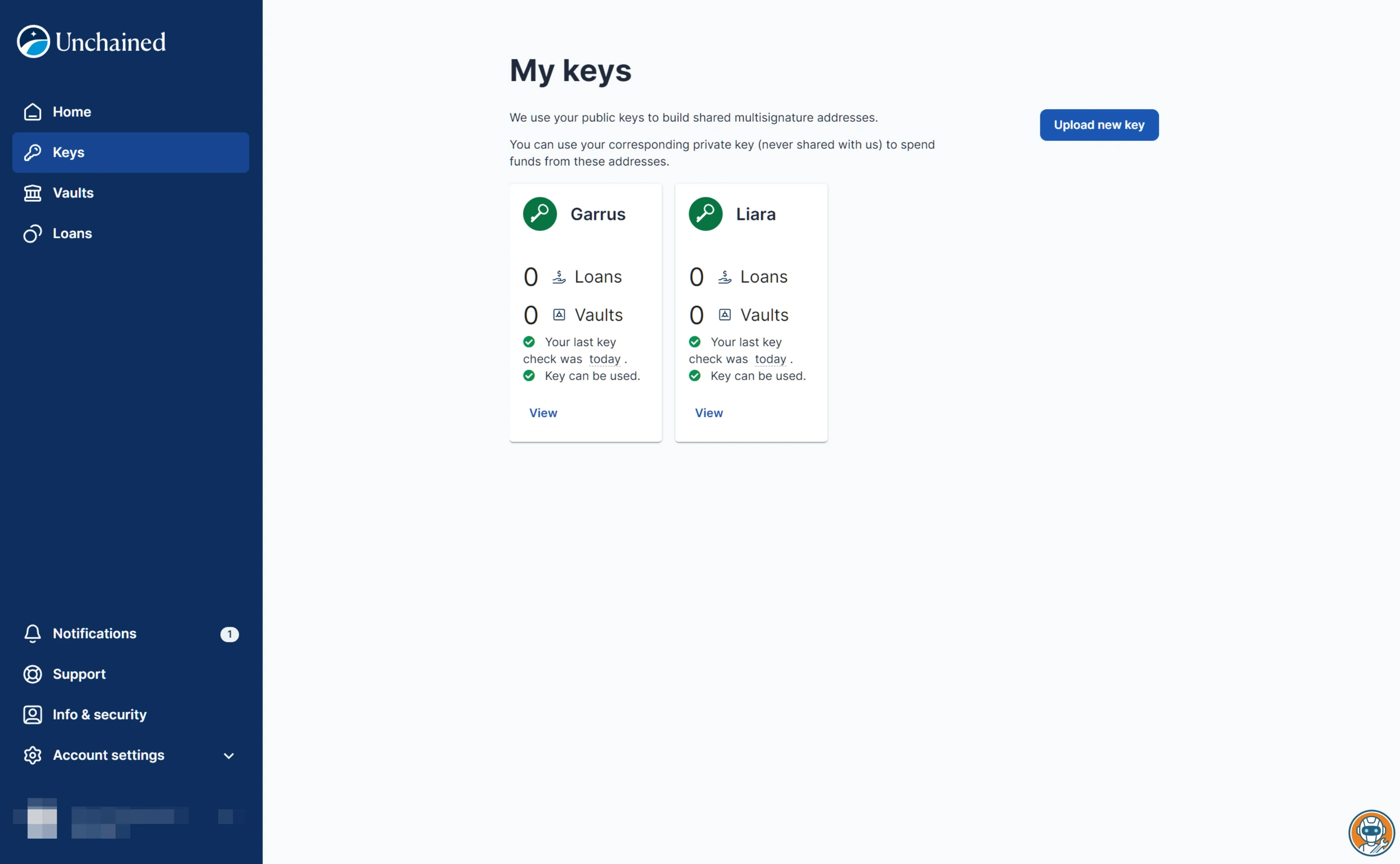

Unchained — For People Who Actually Mean "Not Your Keys"

Every crypto IRA article says the words "not your keys, not your crypto." Then they recommend platforms where a company holds all your keys. Unchained is the only IRA provider where you actually hold your own private keys through a collaborative multisig vault. Two of three keys required to move funds, and you hold two of them.

Only IRA where you hold your own keys via 2-of-3 multisig — your Bitcoin survives even if Unchained disappears.

Anyone wanting altcoins or low fees — it is Bitcoin-only with a $250/yr fee and 1.5% per purchase.

- True self-custody — you hold 2 of 3 multisig keys

- Bitcoin survives even if Unchained goes bankrupt

- No counterparty risk on the custody side

- Supports Traditional, Roth, SEP, and Inherited IRAs

- Bitcoin only — zero altcoin support

- $250/year account fee plus 1.5% conversion fee on purchases

- $2,000 minimum per trade

- Steeper learning curve — you're managing hardware wallets

The fee structure is real. $250 per year in account fees, 1.5% on every bitcoin purchase, plus you'll want to buy two hardware wallets (~$75 each). For a $10,000 IRA, that's roughly 4% in first-year costs. Expensive.

But here's why the r/Bitcoin crowd doesn't care about those fees: if iTrustCapital's custodian gets hacked, your crypto is gone and you're filing insurance claims. If Unchained disappears tomorrow, you have two hardware wallets with your Bitcoin on them. You just import the keys into a new wallet and move on. That's not marketing copy. That's how multisig actually works.

This isn't for everyone. You need to be comfortable managing hardware wallets, understanding UTXO management, and paying a premium for sovereignty. But for the subset of people who got into Bitcoin specifically because of self-custody principles, compromising on that for retirement savings feels wrong. Unchained is the only IRA that doesn't ask you to compromise.

Use Unchained if self-custody is non-negotiable and you're Bitcoin-only. Skip it if you want altcoins, low fees, or a simple setup.

Bitcoin IRA — The Name Brand With Predatory Fees

I've been putting off writing this section because it's going to sound harsh. But the numbers don't lie.

Longest track record since 2016 with $250M BitGo insurance — but that is where the advantages end.

Everyone — the 5.99% setup fee plus 2% trading fee plus monthly maintenance makes it mathematically indefensible.

- Founded 2016 — longest track record in the space

- 75+ cryptocurrencies supported

- $250M BitGo insurance coverage

- 200,000+ users — large user base

- 5.99% setup fee on deposits — the highest in the industry

- 2% trading fee — double most competitors

- 0.08% monthly maintenance fee that never stops

- Fee structure is deliberately opaque — multiple users report unexpected charges

- Trustpilot flagged their review practices as potentially biased

Let's do the math on a $25,000 deposit. Day one: you lose $1,497.50 to the setup fee. Then you buy Bitcoin, another 2% gone, so $470 in trading fees. Then you pay $20/month in maintenance fees, which is $240/year. After one year of just holding, you've paid roughly $2,200 in fees. That's 8.8% of your investment, gone, before your Bitcoin has earned a single dollar.

On iTrustCapital, that same $25,000 costs you $250 in first-year trading fees (assuming one buy). On Fidelity, about the same. The difference over 10 years, with compounding, is staggering.

One RetirementLiving.com reviewer put it bluntly: "Very very very expensive, that's why they don't tell you the fees up front." Another reported "buying fees of 5% and selling fees of 3%." A third user who invested $1,000 lost 60% to fees and spent 2.5 months trying to close the account. Trustpilot itself flagged that Bitcoin IRA "may be asking for reviews in a way that Trustpilot doesn't support."

Bitcoin IRA ranks on competitor lists because their affiliate payouts are among the highest in the industry. That's the quiet part out loud.

Skip Bitcoin IRA. There is no scenario where paying 5.99% upfront plus 2% per trade plus monthly fees makes mathematical sense when iTrustCapital charges 1% with no other fees.

The ETF Question: Do You Actually Need a Crypto IRA?

This is the section no crypto IRA review will write because it kills their affiliate commissions. But I think about it constantly.

BlackRock's IBIT charges 0.25% per year. Fidelity's FBTC charges 0.25%. Bitwise's BITB charges 0.20%. You can buy any of these in a standard Roth IRA at Fidelity, Schwab, or Vanguard. No special account needed. Spot Ethereum ETFs exist too (ETHA, FETH). And Fidelity just launched FSOL for Solana exposure.

So if your plan is "buy Bitcoin and hold for 20 years," a spot Bitcoin ETF in a regular Roth IRA is objectively the cheapest path. You're paying 0.25% annually instead of 1% per trade. Over 20 years on a $50,000 portfolio earning 10% annually, that fee difference costs you approximately $28,000. That's not a rounding error.

You need a dedicated crypto IRA if:

- You want altcoins (Solana, Chainlink, Arbitrum, etc.) beyond what ETFs cover

- You want to trade actively inside the IRA, 24/7 trading, no market hours

- You want actual self-custody of your Bitcoin (Unchained)

- You want to own the underlying crypto, not ETF shares representing crypto

You don't need a crypto IRA if:

- You're just buying Bitcoin or Ethereum and holding long-term

- You already have a brokerage IRA at Fidelity, Schwab, or Vanguard

- Fee minimization matters more than token selection

Honestly? About 70% of the people searching "best crypto IRA" would be better served buying IBIT in their existing Roth IRA and saving thousands in fees over the next decade. I'm not going to pretend otherwise.

The Hidden Spread Nobody Talks About

Every crypto IRA platform advertises a trading "fee." What they don't advertise is the spread, the difference between the price you see and the price you actually get. A 1% advertised fee with a 0.5% spread means you're really paying 1.5%.

iTrustCapital routes through institutional liquidity providers. Their spread is typically tight, reports suggest 0.1-0.3% on major pairs. Fidelity bakes the spread into their 1% (it's technically all spread, no "fee"). Alto routes through Coinbase, so you get Coinbase's institutional spreads. Unchained converts through their own trading desk and the 1.5% fee is all-in.

Bitcoin IRA's spread is where things get ugly. Multiple users report that the actual execution price deviates 3-4% from market price. Combined with the 2% stated trading fee, you can lose 5-6% on a single round trip (buy + sell). On a $10,000 trade, that's $500-600 gone.

If a platform won't publish a full fee schedule with spread data, assume the spread is the profit center. That's not cynicism, that's how crypto OTC desks work.

Frequently Asked Questions

One to Watch: Crypto.com IRA

Crypto.com launched its IRA product on March 3, 2026. Official help pages now show no setup, monthly, or maintenance fees, a $60 termination fee, a match program with holding-period rules, and access to crypto plus stocks and ETFs. On paper, this is the most aggressive mixed-asset offering in the market.

Not moving it to the main rankings yet because the public IRA-specific evidence is still thinner than the marketing. The contribution match has a four-year holding period, and early withdrawals or transfers can trigger a reversal. The narrower Crypto.com IRA vs iTrustCapital comparison breaks down the match-versus-fee clarity tradeoff. For now, I would treat it as a serious contender that needs more operating history.

The Bottom Line

For most people: iTrustCapital . Cleanest fee structure in the industry, no monthly garbage, 90+ tokens. It's the default recommendation because nothing else matches the fee-to-feature ratio. Your IRA contributions have annual limits. Every dollar lost to fees is a dollar that can never compound tax-free again. iTrustCapital respects that.

Already have a Fidelity account? Just use Fidelity Crypto IRA for BTC/ETH/SOL and skip the hassle of opening a new account entirely. Combine actual crypto with spot ETFs in one place.

Bitcoin maximalist who won't trust a custodian? Unchained . Pay the premium. Sleep at night.

Need 250 altcoins? Alto . $10 minimum, same 1% fee as iTrustCapital, massive Coinbase-powered token list.

Bitcoin IRA? Hard pass.

And honestly, before opening any crypto IRA, check whether a spot Bitcoin ETF in your existing Roth IRA does the same job for a quarter of the cost. For a lot of people, it does. The crypto tax implications are simpler too.

If you're already managing crypto across multiple platforms, a portfolio tracker helps you see the full picture before moving anything into an IRA. And if security is keeping you up at night, the right hardware wallet is step one, whether it's for an Unchained multisig vault or just holding your non-IRA crypto properly.

Ready to check iTrustCapital?

Use the verified route if the trade-offs still fit. If not, jump back to the summary and compare the alternatives.

Crypto and productivity editor focused on cost, custody risk, setup friction, exports, fees, and workflow drag. Prioritizes verifiable numbers and clear skip criteria over hype.

Lucas starts with total operating cost, then ranks tools by setup and recurring friction, custody or export, reversibility, and whether the decision still makes sense when the exit path is included.

Related Articles

Stablecoin Cards Compared: Rewards, FX, and Custody Traps

Stablecoin-funded payment cards compared by everyday spend cost, reward caps, FX and conversion fees, custody model, region availability, and tax friction

Coinbase Card, Bybit Card, Crypto.com Prepaid Card, and Nexo Card compared by stablecoin spend cost, rewards, FX fees, custody, and region fit.

MoonPay vs Transak vs Ramp: Which Crypto On-Ramp Costs Less?

3 crypto fiat on-ramp providers compared by fee clarity, payment rails, wallet delivery, partner markup risk, and buyer fit

MoonPay, Transak, and Ramp Network compared by official fee disclosures, payment rails, partner markups, KYC caveats, and wallet-delivery fit.