Crypto.com IRA vs iTrustCapital looks like a clean account-bill fight at first. Crypto.com has a zero recurring account charge and a match. iTrustCapital has the boring 1% crypto transaction line. That framing misses the real decision.

My default pick is iTrustCapital for most crypto IRA buyers. Not because the product is exciting. Because an IRA decision should be easy to model over years, and the bill story is cleaner from public evidence.

Crypto.com's IRA is the more aggressive offer. It combines crypto, stocks, ETFs, staking language, and a contribution match inside the Crypto.com app. That is interesting. It is also exactly why I would slow down before moving retirement money there.

That matters.

This is an evidence-led comparison. I checked official sources on May 13, 2026, captured rendered screenshots, reviewed current SERPs, looked at limited public r/Crypto_com and r/Bitcoin threads, and verified the commercial routes. I did not open accounts, submit KYC, fund an IRA, initiate a rollover, place trades, stake assets, withdraw funds, or contact support.

If you are still choosing the wider shortlist, start with our best crypto IRAs guide. If this is not retirement money, the crypto exchanges guide is the better first decision. And if you are leaning toward Unchained because key control matters, read the hardware wallet comparison before you treat self-custody as a slogan.

-

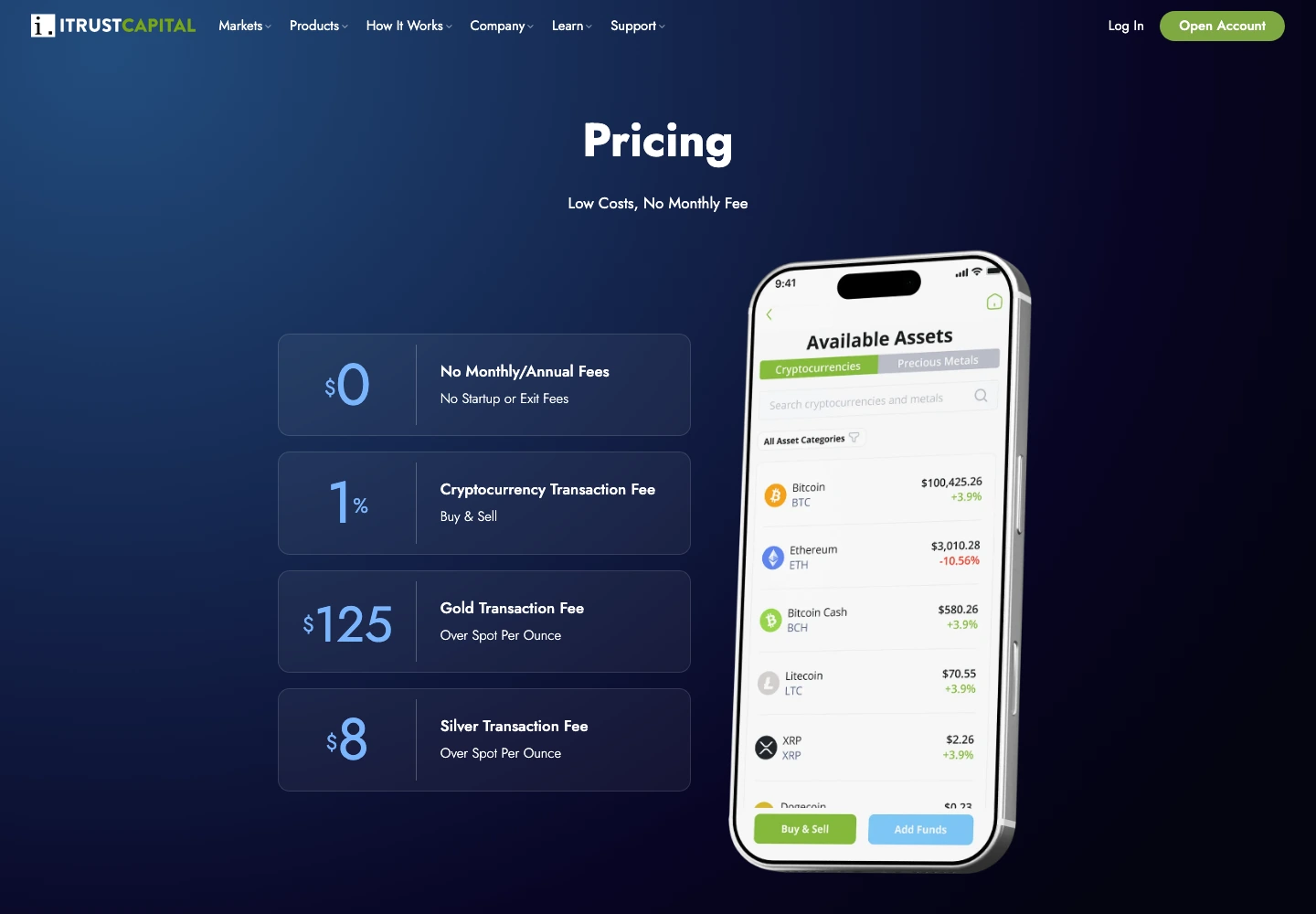

#1 iTrustCapitalBest default for most crypto IRA buyers: public 1% crypto transaction fee and no recurring account fee on the pricing page

-

#2 Crypto.com IRABest if you want crypto, stocks, ETFs, and a conditional IRA match in one app

-

#3 Unchained IRABest Bitcoin-only control pick: collaborative custody, higher fees, and a more demanding setup

If a friend asked me where to start, I would send them to iTrustCapital first and make them write down the exact fee model. If they were already deep in the Crypto.com app and wanted stocks, ETFs, crypto, and a match in the same IRA wrapper, I would have them compare Crypto.com IRA . If they were Bitcoin-only and allergic to custodial key control, I would tell them to study Unchained slowly.

The decision is match discipline, not the launch headline

A zero recurring account charge is useful. A match can be useful. But retirement accounts punish sloppy assumptions because every tiny drag or lock-in rule has time to compound.

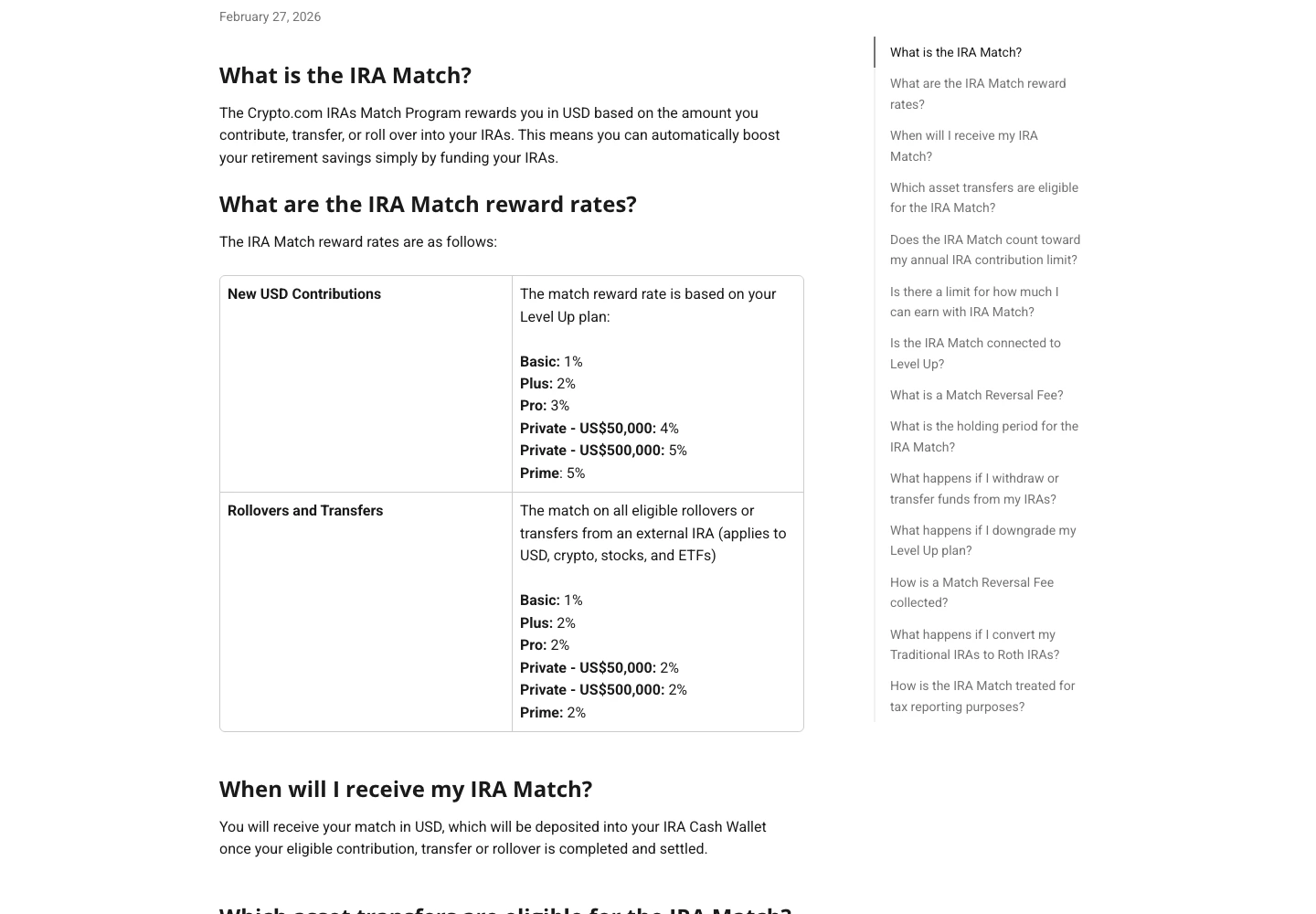

The Crypto.com offer has two real attractions. First, its IRA help page says there are no setup, monthly, or maintenance fees, with a $60 termination fee if you close the IRA. Second, the IRA Match page shows a match from 1% to 5% on new USD contributions depending on Level Up plan, and 1% to 2% on eligible rollovers and transfers.

That is the hook. The catch is the holding period. Crypto.com says matched contributions, transfers, and rollovers must stay in the IRA for at least four years from the deposit date. A higher Level Up match also has a one-year Level Up holding requirement. Withdraw or transfer early and a Match Reversal Fee can apply.

So the match is not a coupon. It is a behavior contract.

iTrustCapital is less flashy. Its public page shows $0 monthly or annual charges, $0 startup or exit charges, and a 1% cryptocurrency transaction line for buys and sells. Its help page says the same 1% applies to digital asset purchases and sales. That makes the bill easier to explain before signup.

Small detail.

Easy-to-explain costs are underrated in retirement accounts. You do not need the most exciting platform. You need the one whose bill you can still explain after three market cycles.

Crypto.com IRA vs iTrustCapital vs Unchained

| Feature | iTrustCapital | Crypto.com IRA | Unchained IRA |

|---|---|---|---|

| Best job | Default crypto IRA for simple fee modeling | Mixed crypto, stock, and ETF IRA inside one app | Bitcoin-only IRA for key-control buyers |

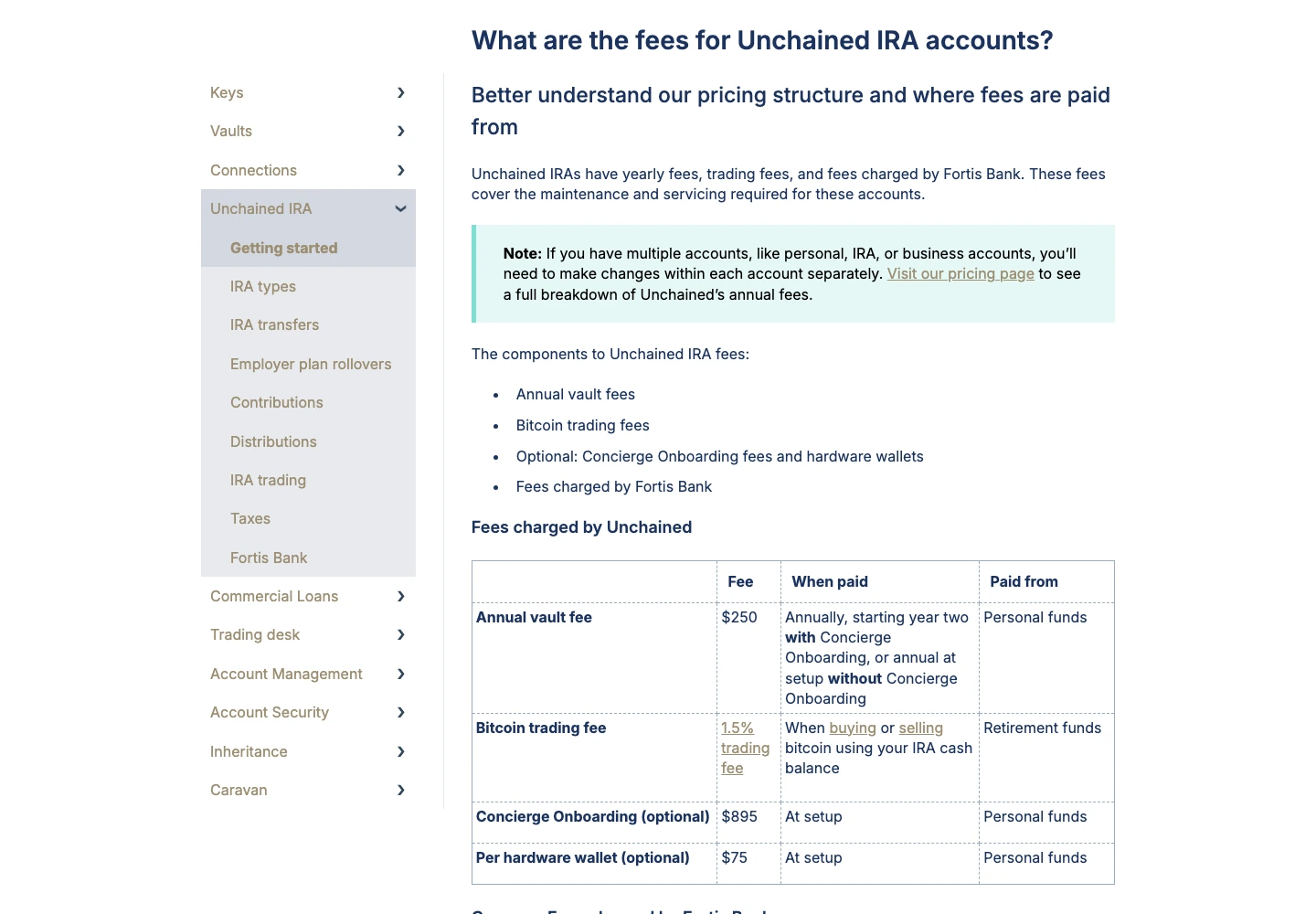

| Public bill proof | $0 monthly/annual/startup/exit charges and 1% crypto transaction line | $0 setup/monthly/maintenance charges; $60 termination charge | $250 annual charge starting year two and 1.5% bitcoin trading line |

| Crypto bill | 1% on digital asset buys and sells | App trading flow; public IRA help pages do not give one flat crypto fee | 1.5% bitcoin conversion fee; optional hardware and concierge costs |

| Asset scope | Crypto plus physical gold and silver | 400+ cryptocurrencies and 12,000+ stocks/ETFs | Bitcoin only |

| Custody/control | Qualified custodian and institutional storage providers | SIPC for stocks/ETFs; private insurance language for crypto, not SIPC | Collaborative custody with user key control |

| Biggest catch | No self-custody; you rely on the IRA custody structure | Match terms and four-year holding period can change the real value | More expensive and more operationally demanding |

| Action | Compare iTrustCapital | Compare Crypto.com | Compare Unchained |

How I ranked the IRA decision

The ranking uses one shared rubric: Bill Clarity, Match Value, Asset Breadth, Custody Trust, and Retirement Fit. Bill Clarity asks whether the account math is visible before signup. Match Value asks whether incentives are valuable after holding-period rules. Asset Breadth asks whether the product fits the portfolio job. Custody Trust asks what public evidence supports the custody story. Retirement Fit asks whether the setup still makes sense when the account is supposed to last for years.

The ranking is not "highest match wins." That would be lazy. A match can be real and still be the wrong center of gravity if it pushes a reader toward a platform before they understand trade execution, custody limits, insurance limits, tax treatment, and withdrawal rules.

Not close.

iTrustCapital wins because the bill model is simpler from public evidence. Crypto.com IRA is the more ambitious product, and it could become the better answer for some app-first buyers. Unchained is not trying to beat either on breadth or cheapness. It is the sovereignty pick for Bitcoin people who mean it.

1. iTrustCapital: the better default when the bill must be obvious

iTrustCapital's advantage is not that 1% is tiny. It is that the 1% is easy to find and easy to model. The public page shows no monthly or annual account charge, no startup or exit charge, and a 1% cryptocurrency transaction line for buys and sells. Official help documentation repeats that all digital asset purchases and sales incur a 1% transaction charge.

That does not make iTrustCapital perfect. You do not control the keys. iTrustCapital says it is a software platform and that IRA custody uses a third-party qualified custodian, Fortis Bank, with institutional storage providers including Fidelity Digital Assets, Coinbase Custody, and Fireblocks. That is a custody chain, not self-custody.

For most buyers, that tradeoff is acceptable because they are using an IRA wrapper for tax treatment and administration. If the goal is a simple crypto IRA with a visible transaction fee and no recurring account fee from the public pricing page, iTrustCapital is still the cleaner default.

The public pricing page makes the core crypto bill easy to model: no recurring account fee on the page and a 1% transaction fee for buys and sells.

Skip it if self-custody is non-negotiable, if you want stocks and ETFs in the same app, or if you need advice rather than a self-directed IRA platform.

iTrustCapital ranks first because fee clarity is the most important buyer job for this keyword. The accepted tradeoff is custodial key control.

- Public pricing page shows a 1% crypto transaction fee

- No monthly, annual, startup, exit, storage, withdrawal, or transfer charge on the public table

- Crypto plus physical gold and silver fits the alternative-asset IRA buyer

- Custody documentation gives a concrete qualified-custodian and storage-provider chain

- No self-custody of IRA crypto

- A 1% trade fee is still expensive for frequent trading

- Does not solve whether a crypto IRA is better than a spot ETF inside a normal brokerage IRA

- This comparison did not verify account approval, live spread, transfers, support, or withdrawals hands-on

2. Crypto.com IRA: the better app-first offer, but read the match like a contract

Crypto.com IRA is the more interesting product. Official help pages say the account can hold crypto, stocks, and ETFs. The investing page says Crypto.com IRAs provide access across more than 12,000 stocks and ETFs and more than 400 cryptocurrencies from the Crypto.com app. The overview page says there are no setup, monthly, or maintenance charges, with a $60 termination charge.

The match is the reason many readers will click. Crypto.com's match page shows 1% to 5% for new USD contributions depending on Level Up status, and 1% to 2% on eligible rollovers or transfers. It also says the match does not count toward the annual IRA contribution limit.

Sounds great. Now the fine print: matched funds have a four-year holding period, and withdrawals or transfers can trigger a Match Reversal Fee. If a higher match came from Level Up status, there is also a one-year holding rule. That does not make the offer bad. It makes it conditional.

The other reason to slow down is crypto trade visibility. Crypto.com's IRA investing page explains that crypto trading in the IRA works like regular trading in the Crypto.com app, with the IRA selected as the receiving account. I did not find a single public IRA-specific flat crypto transaction line comparable to iTrustCapital's 1% line. That means I would treat app order previews as mandatory before funding.

Crypto.com also has a custody nuance. Its overview says SIPC protection applies to stocks and ETFs, while crypto assets are protected by privately placed insurance and are not government insured or SIPC insured. That is not a knock. It is the kind of difference a retirement buyer should understand before putting a mixed-asset IRA in one app.

Crypto.com has the most aggressive bundle: crypto, stocks, ETFs, staking language, zero account fees, and a match program in one app.

Skip it if you mainly want a simple crypto-fee model, if the four-year match holding period annoys you, or if app order-preview pricing is not transparent enough for retirement money.

Crypto.com IRA ranks second because the feature set is strong, but the match and crypto trade economics require more buyer discipline than the headline suggests.

- No setup, monthly, or maintenance charges on the official IRA overview page

- Match rates can be meaningful for buyers who can satisfy the holding rules

- Broad asset scope across crypto, stocks, and ETFs in one app workflow

- Official pages separate SIPC treatment for stocks/ETFs from crypto insurance language

- Four-year match holding period can reduce flexibility

- Higher match tiers depend on Level Up plan status and separate conditions

- Public IRA help pages do not show one flat crypto trading line like iTrustCapital

- Newer IRA product with thin public IRA-specific community evidence

3. Unchained IRA: the right loser for Bitcoin-only key control

Unchained loses a normal fee comparison and still belongs here. It is not trying to be the cheapest multi-asset IRA. It is trying to solve the "not your keys" problem inside a Bitcoin IRA.

Official Unchained documentation shows a $250 annual vault charge starting year two, a 1.5% bitcoin trading line, optional $895 concierge onboarding, and optional $75 hardware wallets. Its Bitcoin IRA page also says the IRA is Bitcoin-only and uses a structure where you keep control of keys through a vault workflow.

That bill stack is not small. On a $7,500 annual contribution, a 1.5% conversion line is $112.50 before any account charge or hardware purchase. If you are buying tiny amounts, Unchained can feel heavy fast.

But the buyer is different. Public r/Bitcoin discussion I checked was not asking for more altcoins. The concrete Unchained walkthrough cared about two-key control, TSP/IRA rollover mechanics, the 1.5% trade desk line, and operational rigidity. That is useful friction, not representative sentiment. It says the real Unchained buyer is willing to accept setup burden for custody control.

Use Unchained if Bitcoin self-custody is the point. Do not use it because you saw "crypto IRA" and assumed every provider is interchangeable.

Unchained is the only pick here whose core value proposition is key control rather than app breadth or low visible fees.

Skip it if you want altcoins, stocks, ETFs, small recurring contributions, a low fixed-cost account, or a hands-off IRA setup.

Unchained ranks third for the broad keyword because it is expensive and narrow, but it is the strongest fit for the Bitcoin-only custody-control buyer.

- Designed around Bitcoin key control instead of custodial convenience

- Official documentation makes annual, trading, concierge, and hardware charges visible

- Strong fit for rollover buyers who specifically want Bitcoin in a retirement wrapper

- Useful contrast against app-first and custodial IRA models

- Bitcoin only

- Higher fixed and trading charges than most broad crypto IRA buyers want

- Operational setup is more demanding than a normal custodial platform

- This article did not test rollover timing, vault setup, trade desk execution, or recovery flow

How to choose without letting the bonus pick for you

Pick iTrustCapital if you want the normal answer. You care about crypto access inside an IRA, you want a published 1% crypto transaction line, and you do not need stocks, ETFs, or self-custody inside the same product. This is the answer I would give most readers because the bill is easiest to explain.

Pick Crypto.com IRA if the match and mixed-asset app really fit your behavior. That means you can live with the four-year match holding period, you understand Level Up conditions, and you are willing to check every order preview before trading crypto inside the IRA. The product is promising. The buyer has to be disciplined.

Pick Unchained if Bitcoin custody is the point of the account. If you are comparing it against iTrustCapital on charges, you are probably not the Unchained buyer. The better question is whether you want a Bitcoin-only IRA badly enough to accept higher bills and more operational work.

The contrarian answer is that some readers should choose none of these. If you only want long-term Bitcoin exposure and already have a brokerage IRA, compare a spot Bitcoin ETF first. It may be boring. Boring is sometimes the leaner answer.

What I would verify before funding

Before sending retirement money to any of these providers, I would make a one-page checklist. Not a spreadsheet with fantasy returns. A boring checklist that says: how money enters, what the order preview shows, who holds the asset, how money exits, and what happens if I change my mind.

For Crypto.com IRA, the first check is the order preview. The public help page explains the app flow, but the buyer still needs to see the actual buy or sell preview before treating the account as cheap. I would also write down the exact match tier, the deposit date, the four-year holding-period date, and the condition that could trigger a Match Reversal Fee. If you cannot explain the match without opening the help page again, you are not ready to fund it.

For iTrustCapital, I would verify the account type, the funding route, and whether the asset list still includes the coins you actually plan to hold. The fee model is cleaner, but a clean fee model does not make every token appropriate for retirement money. It also does not make a custodial IRA the same thing as controlling your own keys.

For Unchained, I would slow down around operations. Two hardware devices, seed backups, inheritance planning, and transaction signing discipline are not side quests. They are the product. If that work sounds annoying, do not buy the self-custody story just because it feels philosophically pure. Start with our seed phrase backup guide and make sure the physical recovery plan is real.

The last check is taxes and exits. Ask what documents you will receive, how Roth conversions are handled, what fees apply if you transfer out, and what happens if you need to unwind the account. None of this is as fun as a match headline. It is the part that keeps a retirement decision from becoming a support ticket with a balance attached.

Final verdict

For most crypto IRA buyers, choose iTrustCapital . It gives the cleanest public bill model in this comparison and keeps the decision focused on the retirement wrapper instead of a promotional match.

The risk is picking the product that looks richest on day one and then discovering the custody model, holding rule, or exit path does not fit how you actually manage retirement money.

Choose Crypto.com IRA if the mixed-asset app, stock/ETF scope, and match are exactly what you want. Just treat the match like a contract, not a discount code.

Choose Unchained if Bitcoin key control matters more than breadth and low fixed charges. That is a smaller audience. It is also a very real one.

Before funding any of them, map the tax workflow. Crypto IRA trades can simplify some tax reporting compared with taxable exchange accounts, but everything outside the IRA still needs clean records. Our crypto tax software guide is the next place to go if your wallets, exchanges, and IRA exposure are starting to overlap.

Frequently Asked Questions

iTrustCapital wins because the core fee model is visible and easier to model before signup. Crypto.com IRA is the more ambitious app-first offer, while Unchained is the Bitcoin-only custody-control specialist.

See pricing